What’s AgTech?

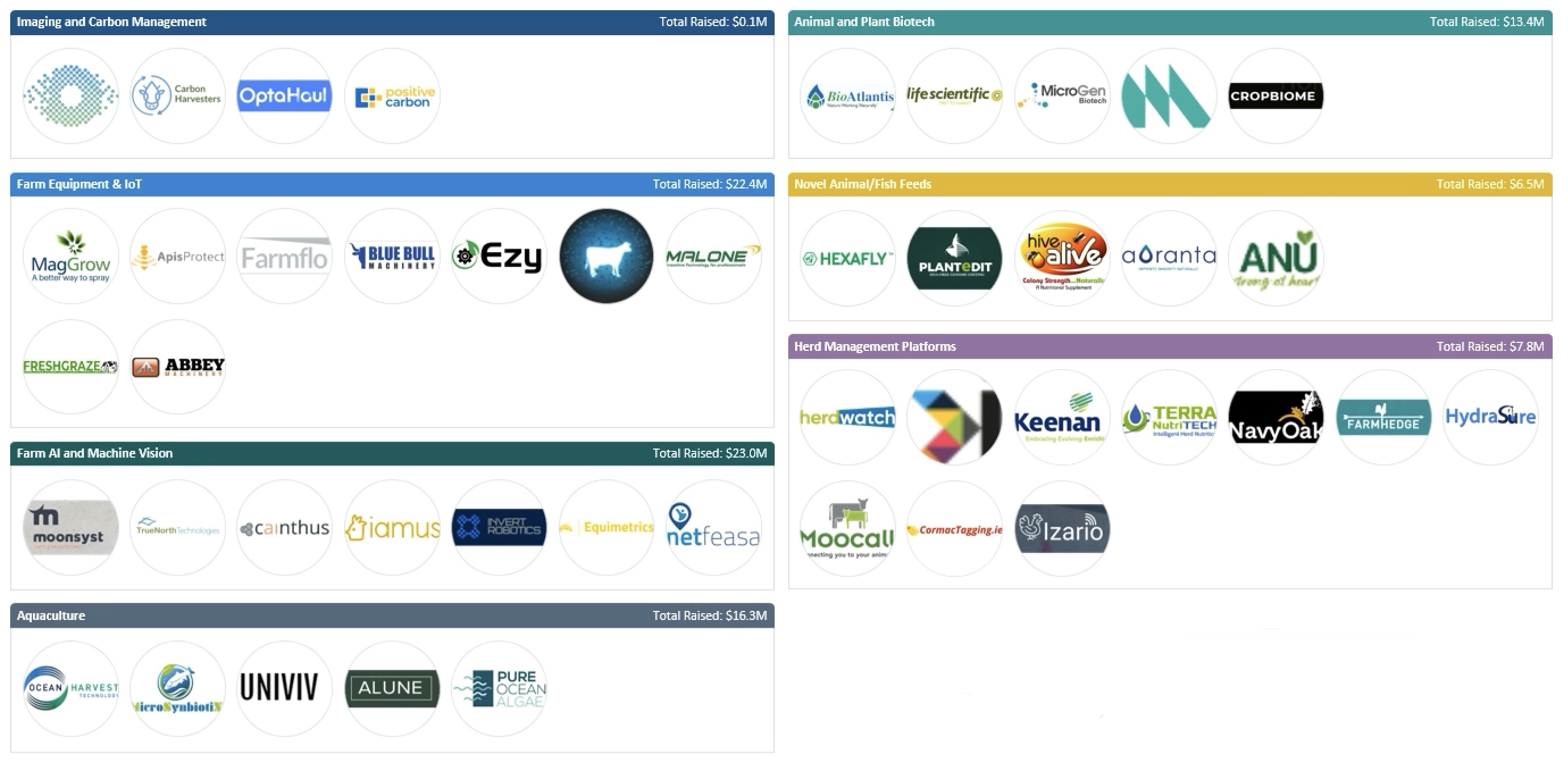

The AgTech sector is aimed at goals that have existed throughout recorded history – yield and efficiency maximisation, enhancement of desirable traits, dealing with pests and, more recently, minimising externalities such as biodiversity loss, climate change and environmental degradation. Globally, AgTech venture activity climbed to over 750 deals accounting for over €10Bn invested last year. In a sign of sector maturation, exits have rapidly increased over the last few years to a record €23Bn realised in trade sales and IPOs in 2021.

What’s happening here?

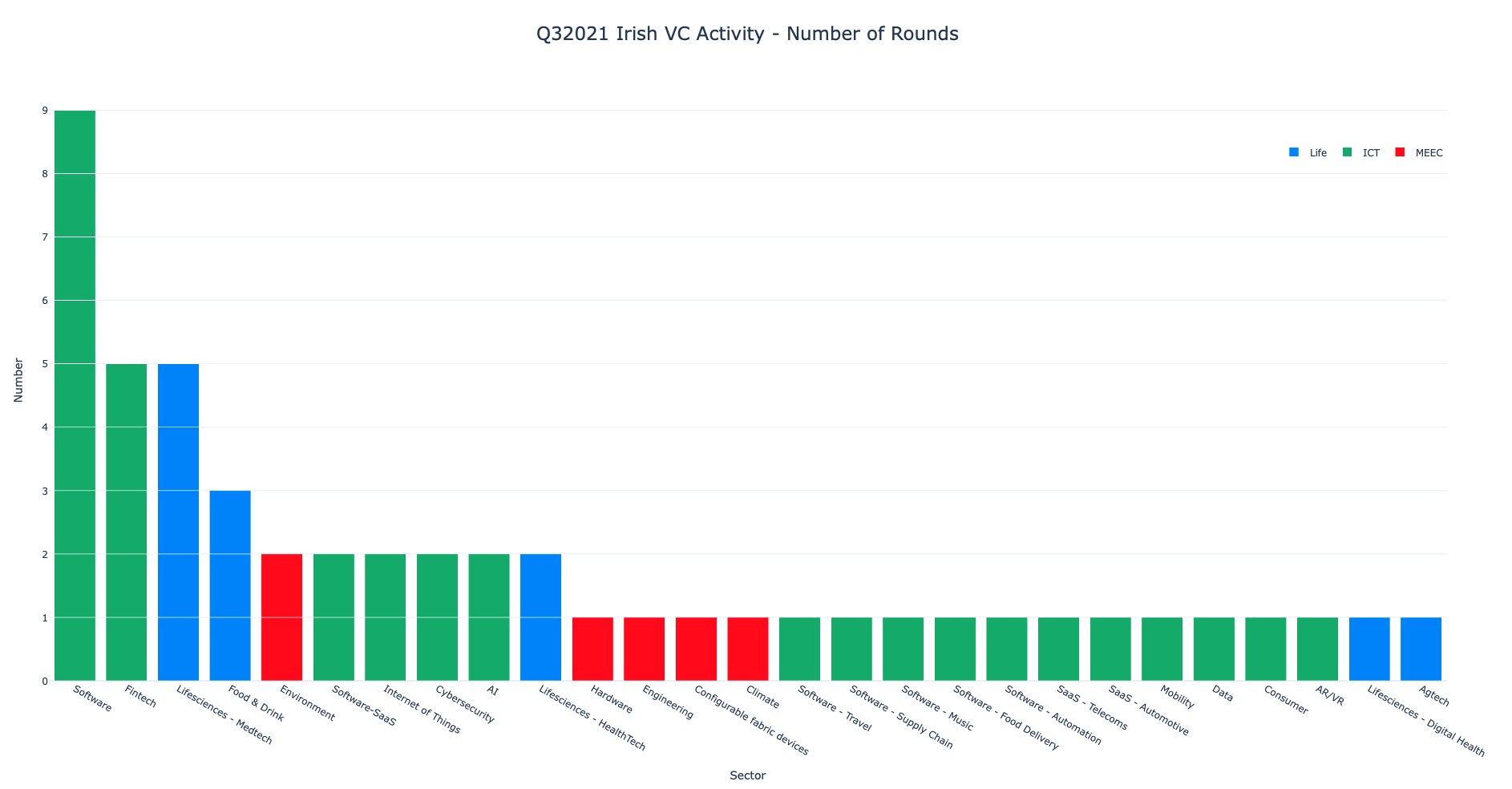

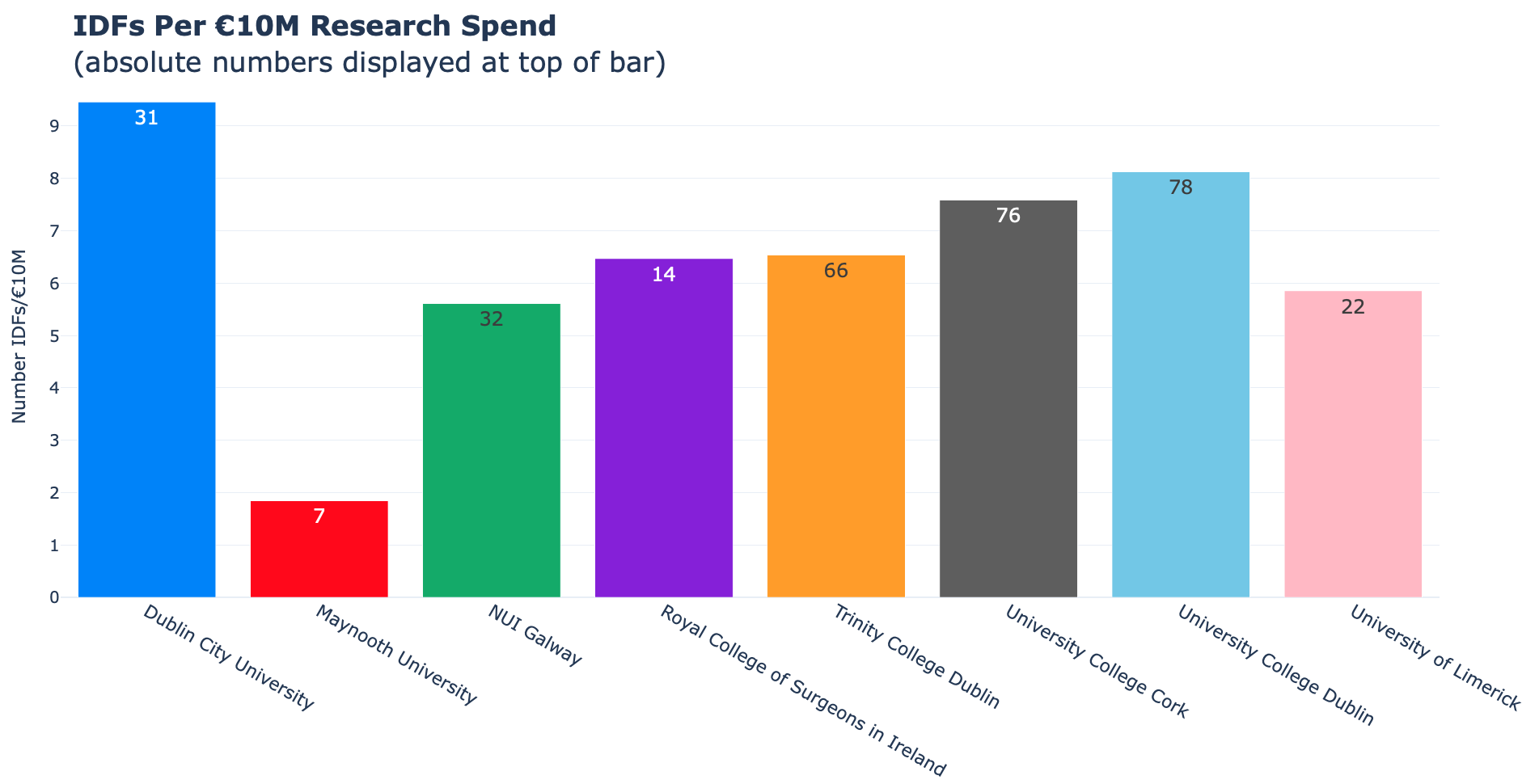

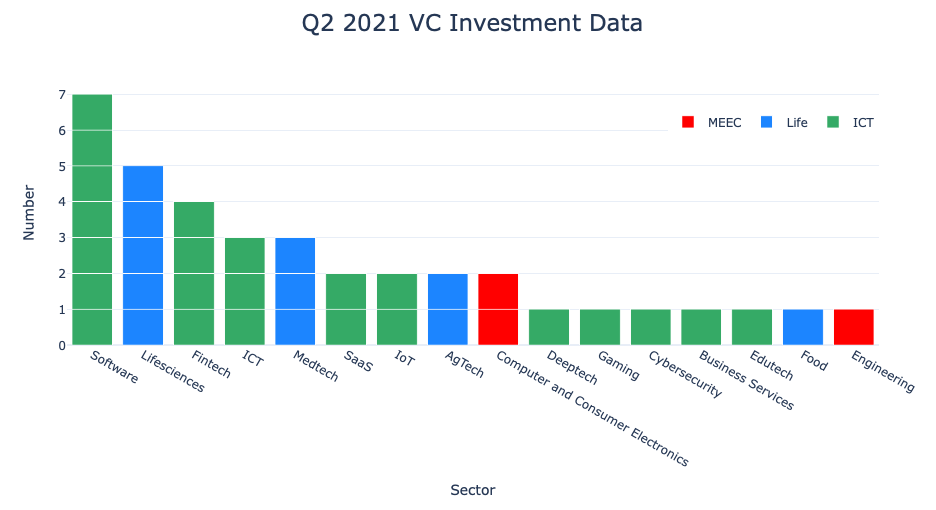

Ireland is ranked third globally in terms of research excellence in Agricultural Sciences (Science Foundation Ireland 2020 Annual Report). The government calls out Climate, Environment and Sustainability in addition to Agriculture, Food and the Marine as major pillars of research to be supported from the €1.9Bn per annum spend within the Irish university R&D ecosystem in its ‘Impact 2030’ strategy. Recent data shows AgriFood companies attracted over €100M in venture investment in 2021 (TechIreland Annual Report and Irish Venture Capital Association data) and there is a growing cohort of start ups and innovative businesses in the space looking to grow and sell globally.

Who are IFC?

The International Finance Corporation is part of the World Bank. IFC’s focus is to develop disruptive technologies by catalyzing entrepreneurship ecosystems via venture capital and growth equity. They operate in developing nations and have great access to local governments and in-country advisors and specialists in addition to capital. IFC is focused on supporting innovative businesses and tech start-ups who are addressing IFC’s development mandates such as climate change, food security, access to health care and education and increasing financial inclusion. See https://www.ifc.org/

What’s the Irish link?

The Ireland Strategic Investment Fund (www.isif.ie) have a strategic relationship with IFC. They are working together to generate growth opportunities for Irish AgTech companies in emerging markets. More information on the collaboration can be found here.

REGISTER: https://www.eventbrite.co.uk/e/irish-agtech-event-with-the-ifc-tickets-347041669977

The webinar is June 7th and a recording will be available afterwards.