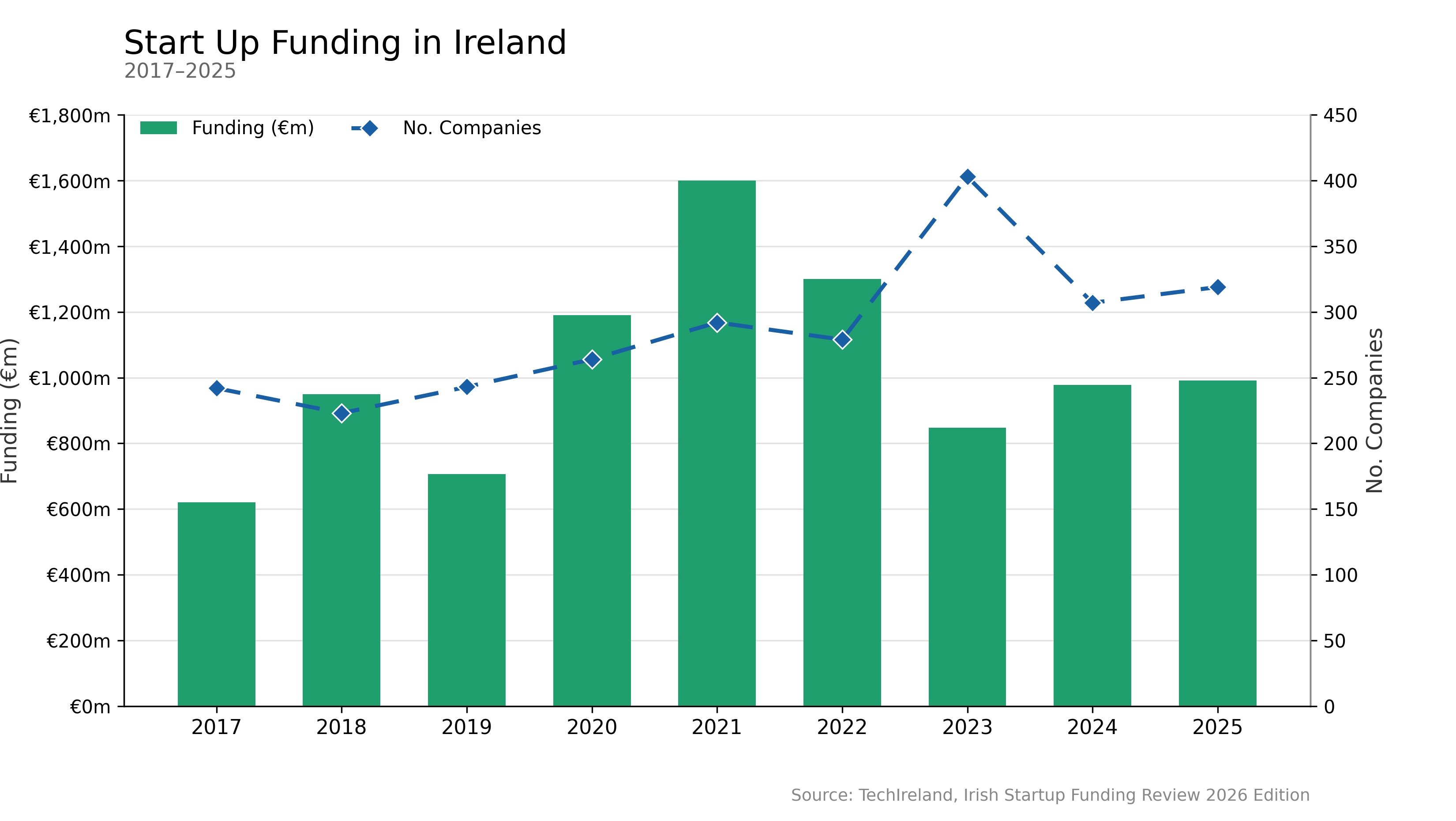

The Irish start up data aggregator, TechIreland, has just published the 2025 start up funding tally. The macro story is one of funding stabilization by cash and number of start ups after falls from the 2021 peak.

Digging into the details, a few things are notable. Just 4 companies account for almost half the funding. Whilst seed rounds of less than a €1m held up well, scaling venture rounds are mostly flat in terms of numbers. So, the pipeline of start-ups and innovation remains strong but the access to scaling finance is one to watch. In that vein, the Irish Venture Capital Association published Q1 2026 venture data this week and report a 58% fall in funding compared with Q1 2025 which is a concern.

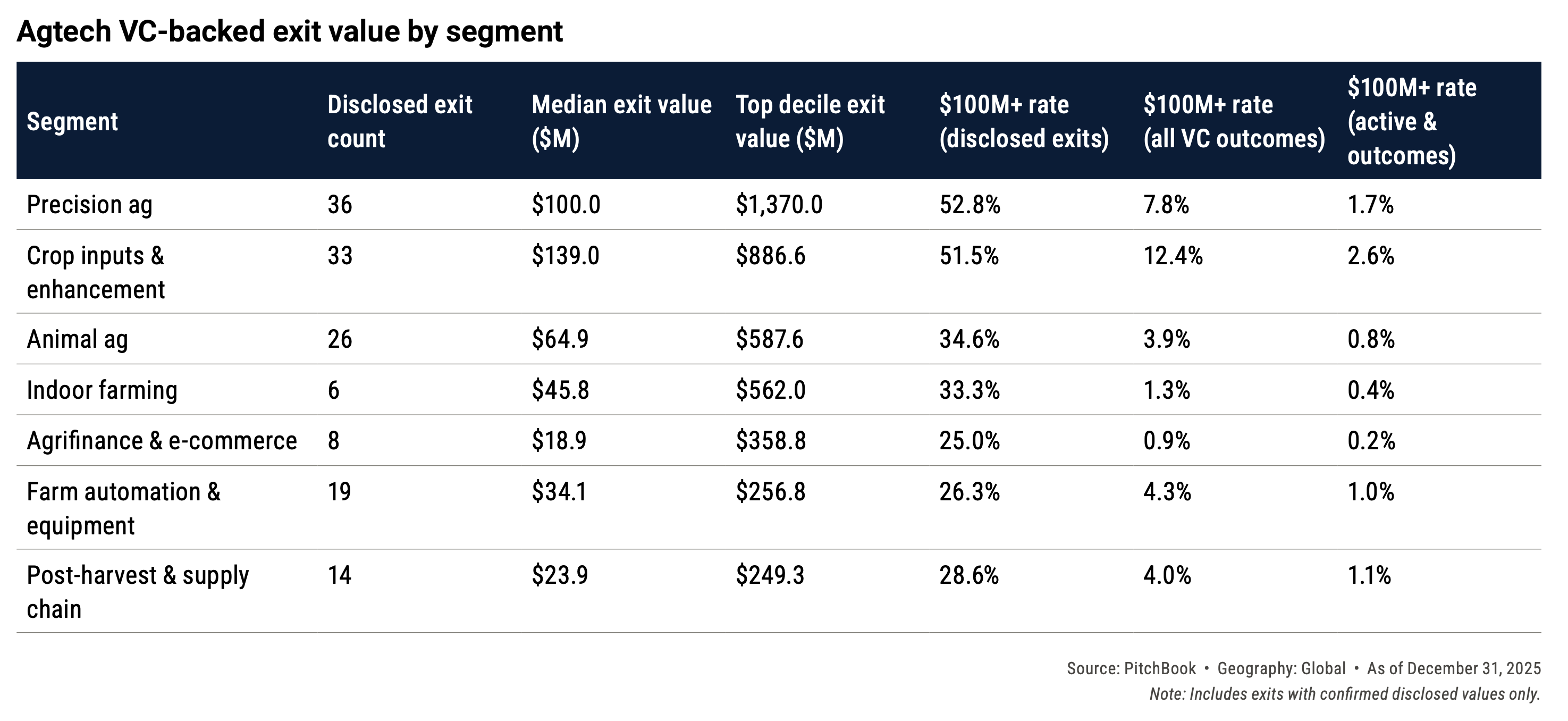

I’ve had a new PitchBook analyst note that reviews some 10 years of AgTech investment data for over a week but not had a chance to say too much about it other than a brief LinkedIn post until now.

Using their own data, Pitchbook survey 1,197 VC-backed agtech companies with known outcomes at end-2025 – 57% are confirmed failures and only 11.9% produced an exit with a disclosed value. Capital destruction sits at a confirmed $8.2bn floor, with 162 failures recorded in 2025 alone — the worst year on record. So it’s not too different to recent posts outlining the many failures to date in this sector. However, the main value in the Pitchbook report is its specificity about where returns can still actually come from and that it’s not all doom and gloom in AgTech.

First, for investors, segment selection drives outcomes more than founder quality or timing. Crop health, precision ag, and animal biotech are the only segments with $100M+ median exits and double-digit exit rates. Biochem & inputs is the standout performer — a 5.7x median exit/raised ratio, an 8% capital destruction rate, and a structurally growing exit market as Bayer, BASF, Syngenta, Novozymes and Corteva all name biologicals as a strategic priority.

Second, for both investors and founders, capital discipline is critical. Companies raising under $1M failed at least 78% of the time, but those raising over $100M before failing destroyed the most capital. The sweet spot is $15M–$60M total raised, exiting at $75M–$200M to a strategic acquirer.

The final insight relates to the last. If a ‘great’ exit looks like $200M, then the timing or stage of an investment is critical to return. Earlier stage investors who have good reserves to maintain their position in the winners are the ones that will see return from their AgTech investments.

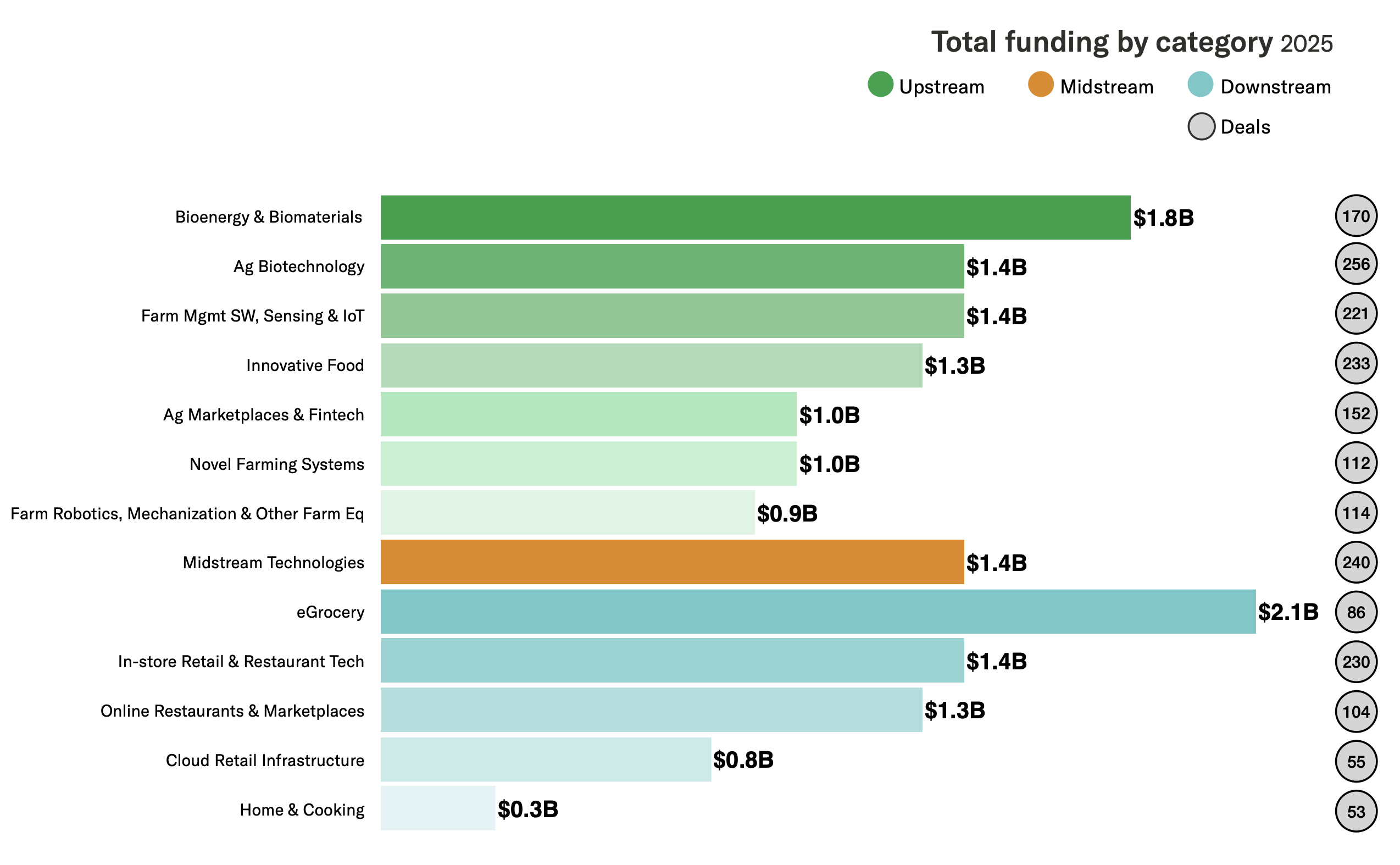

It’s that time of year when the figures are in and various august sources publish the investment data for the year just gone. AgFunder, most especially AgFunder News, have built a good reputation over the years as a source of news on agrifood investment developments from around the wold. Last week their 2025 report came out. Worth a read in its entirety if this is a space of interest. For me, the headlines are that global investment amount totals remain flat or slightly declining over the last 3 years. Countering that, is a real uptick in first time funded new starts which I interpret as a shift from capital keeping existing investments alive after the 2022 carnage to supporting new entrants. On the ‘most active investors’ side, SOSV top the venture rankings by number of investments. Finally – and likely related to the new entrants – is a sense that AI and Robotics is starting to scale in the sector.

Not sure with all the volatility what we can make of the year ahead. With a strong likelihood of inflation ahead throughout the food supply chain, the need for innovation remains high. Assuming this leads to market demand to deploy available interventions immediately, this may favor later stage companies with scaleable solutions get into revenue faster. If this is the case, their attractiveness for acquisition and the associated recycling of capital the space needs to grow might become feasible.

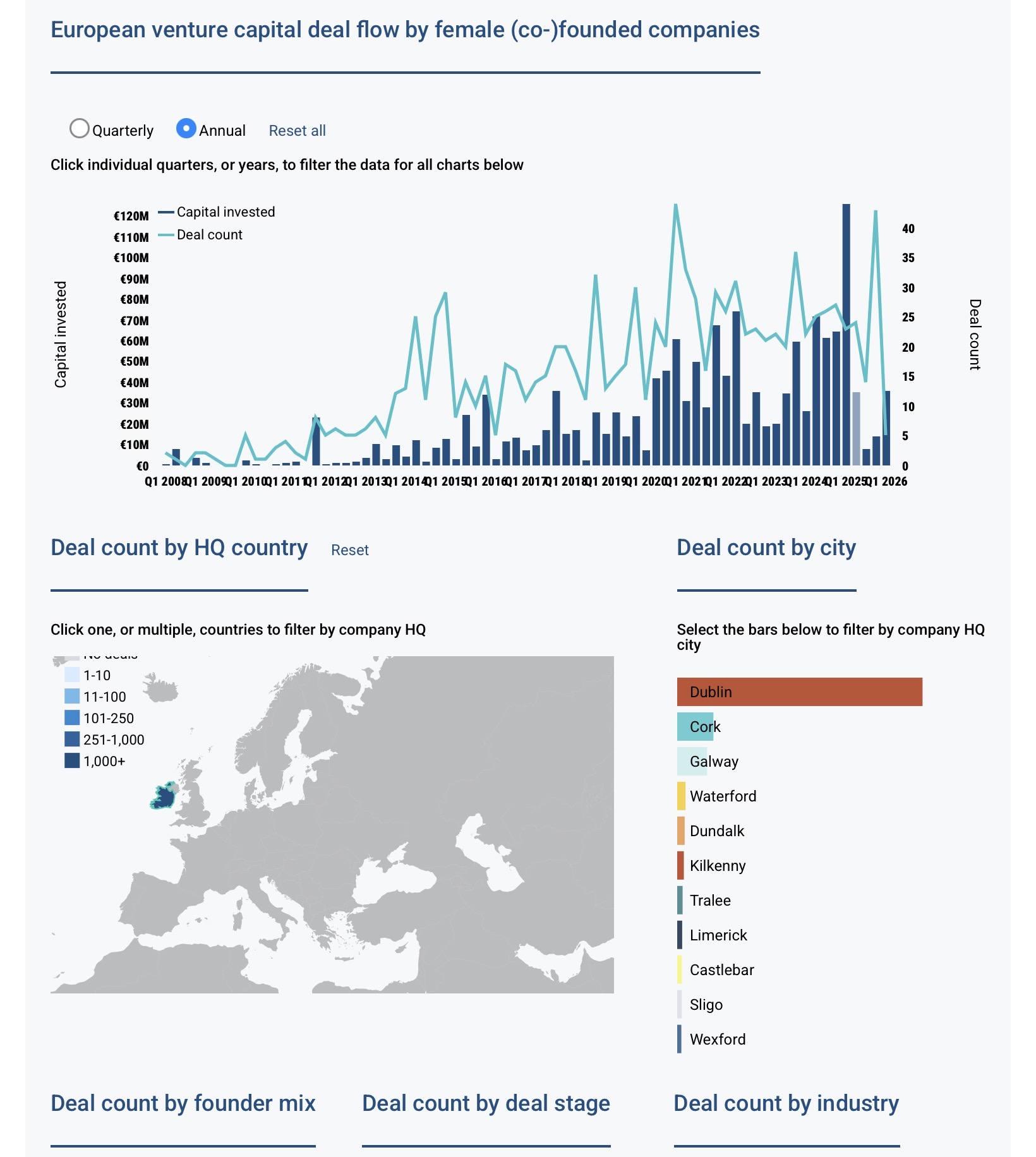

New publicly accessible dashboard from PitchBook on data since 2008 for venture backed female founders. Granular data with filtering by time, stage, industry and location. Data up to end February 2026. Looking at Ireland, a broad trend towards increasing capital allocation over the years.

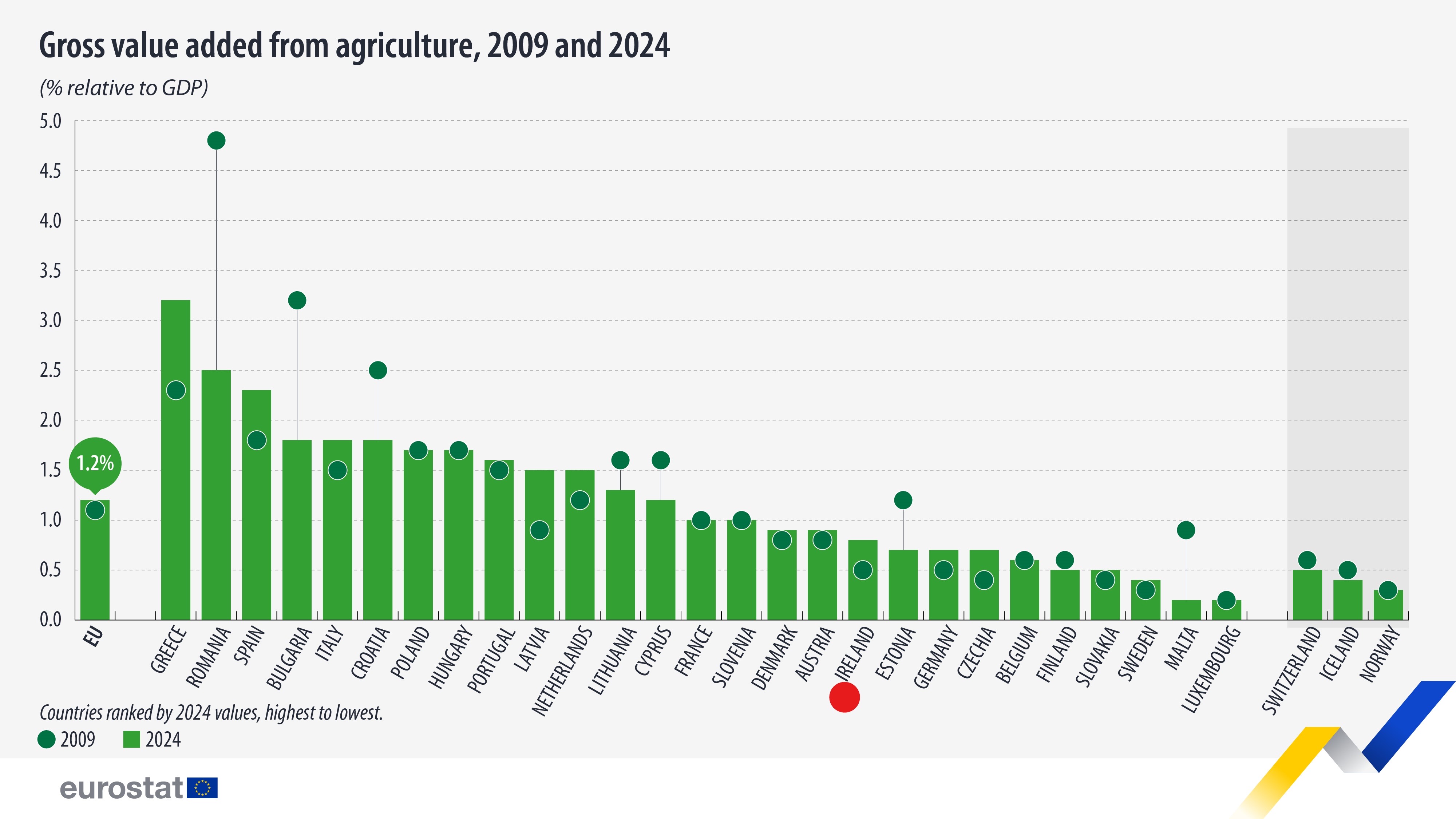

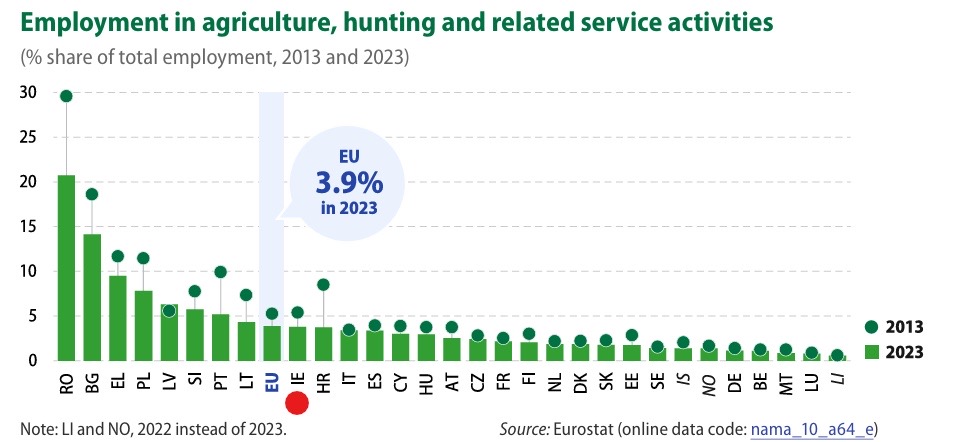

I’m not sure today’s Eurostat figures on the value add of agriculture to the Irish economy do justice to the importance of the sector to the rural economy, normalised as they are to GDP. I think a more illustrative measure, relatively, is the percentage employment of agriculture which is very close to the EU average, albeit declining over the last decade. Original article at https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20260223-1

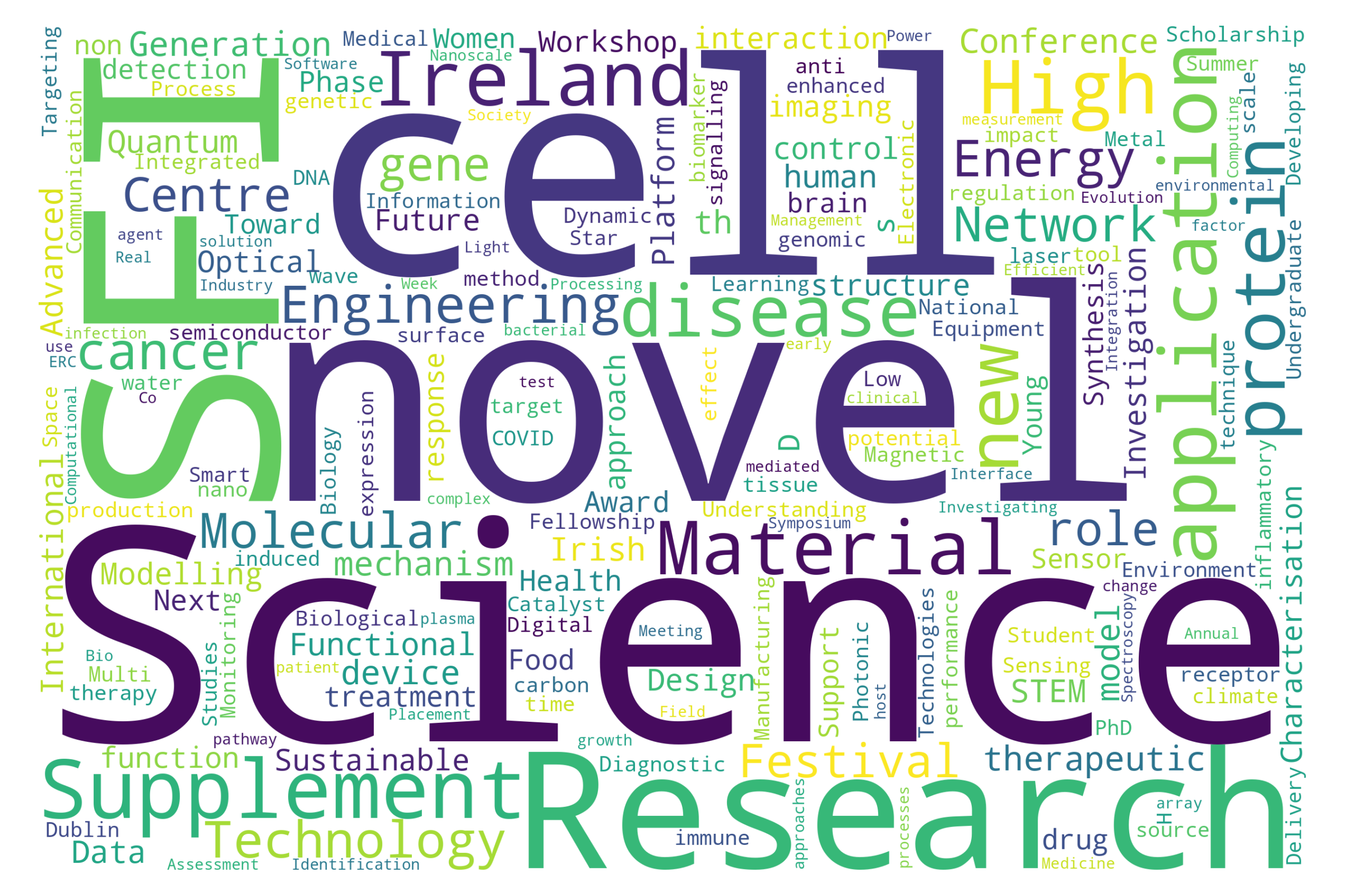

Now that Science Foundation Ireland has become Research Ireland, I came across their updated open data at https://data.gov.ie/ on all the awards they made – over 7200 of them from 2001 to 2025. There are insights here into the evolution of third level research in Ireland and activity around supporting large scale multi-party collaborations and individual commercialisation of promising findings. Latterly, an increasing focus on solving grand challenges is apparent. Too much to distill yet so a quick word cloud of the project titles for now below.

What’s AgTech? The AgTech sector is aimed at goals that have existed throughout recorded history – yield and efficiency maximisation, enhancement of desirable traits, dealing with pests and, more recently, minimising externalities such as biodiversity loss, climate change and environmental degradation. Globally, AgTech venture activity climbed to over 750 deals accounting for over €10Bn invested last year. In a sign of sector maturation, exits have rapidly increased over the last few years to a record €23Bn realised in trade sales and IPOs in 2021.

What’s happening here? Ireland is ranked third globally in terms of research excellence in Agricultural Sciences (Science Foundation Ireland 2020 Annual Report). The government calls out Climate, Environment and Sustainability in addition to Agriculture, Food and the Marine as major pillars of research to be supported from the €1.9Bn per annum spend within the Irish university R&D ecosystem in its ‘Impact 2030’ strategy. Recent data shows AgriFood companies attracted over €100M in venture investment in 2021 (TechIreland Annual Report and Irish Venture Capital Association data) and there is a growing cohort of start ups and innovative businesses in the space looking to grow and sell globally.

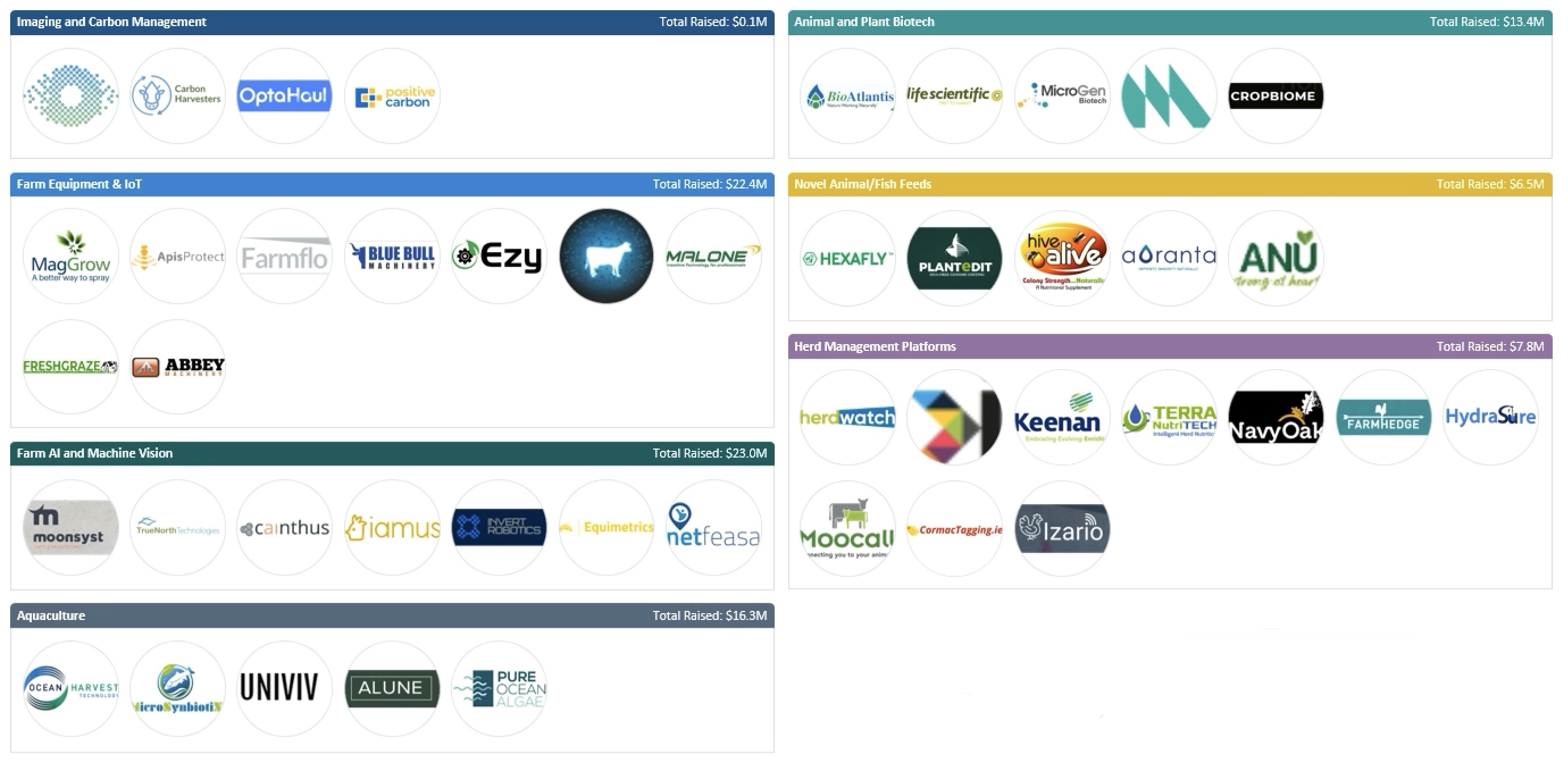

A non-exhaustive list of venture backed AgTech companies in Ireland

Who are IFC? The International Finance Corporation is part of the World Bank. IFC’s focus is to develop disruptive technologies by catalyzing entrepreneurship ecosystems via venture capital and growth equity. They operate in developing nations and have great access to local governments and in-country advisors and specialists in addition to capital. IFC is focused on supporting innovative businesses and tech start-ups who are addressing IFC’s development mandates such as climate change, food security, access to health care and education and increasing financial inclusion. See https://www.ifc.org/

What’s the Irish link? The Ireland Strategic Investment Fund (www.isif.ie) have a strategic relationship with IFC. They are working together to generate growth opportunities for Irish AgTech companies in emerging markets. More information on the collaboration can be found here.