I’ve had a new PitchBook analyst note that reviews some 10 years of AgTech investment data for over a week but not had a chance to say too much about it other than a brief LinkedIn post until now.

Using their own data, Pitchbook survey 1,197 VC-backed agtech companies with known outcomes at end-2025 – 57% are confirmed failures and only 11.9% produced an exit with a disclosed value. Capital destruction sits at a confirmed $8.2bn floor, with 162 failures recorded in 2025 alone — the worst year on record. So it’s not too different to recent posts outlining the many failures to date in this sector. However, the main value in the Pitchbook report is its specificity about where returns can still actually come from and that it’s not all doom and gloom in AgTech.

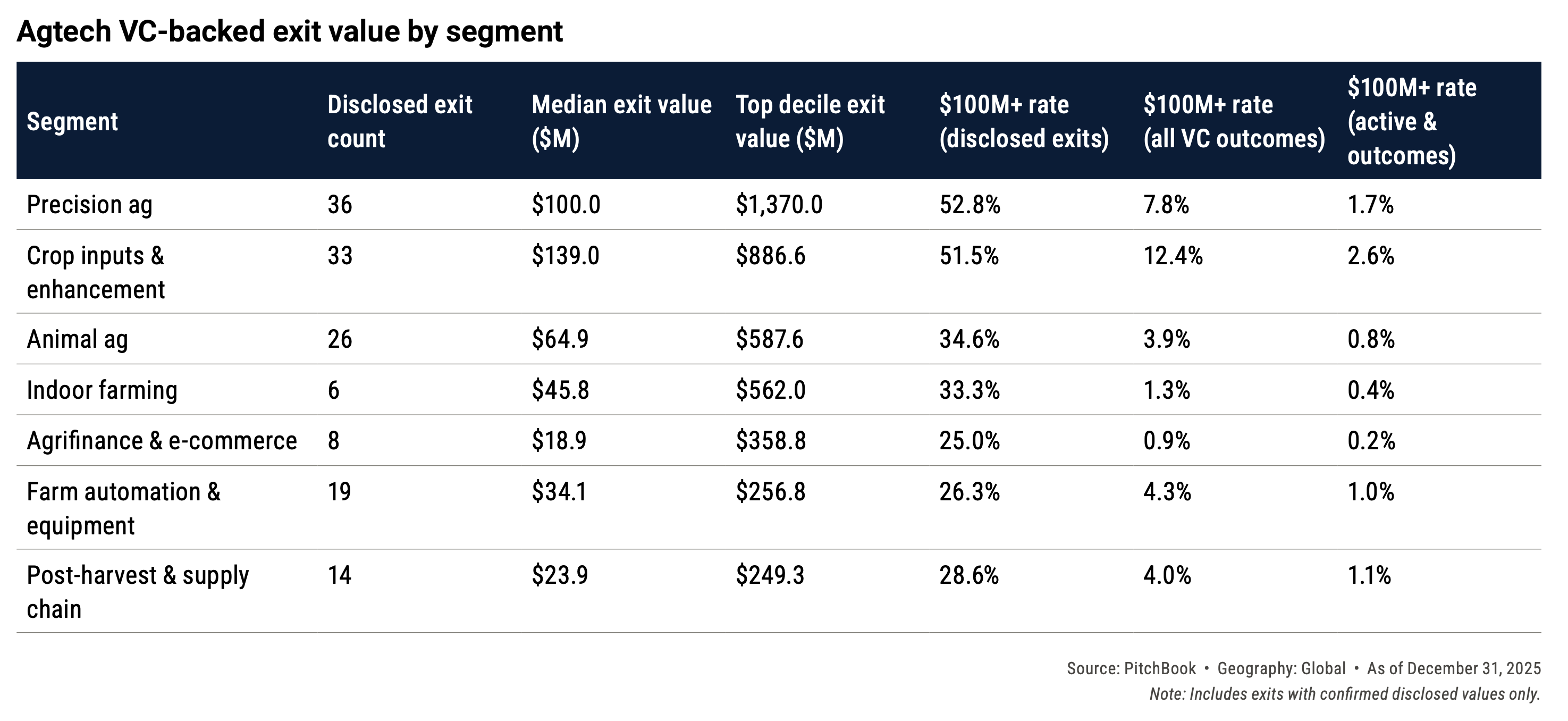

First, for investors, segment selection drives outcomes more than founder quality or timing. Crop health, precision ag, and animal biotech are the only segments with $100M+ median exits and double-digit exit rates. Biochem & inputs is the standout performer — a 5.7x median exit/raised ratio, an 8% capital destruction rate, and a structurally growing exit market as Bayer, BASF, Syngenta, Novozymes and Corteva all name biologicals as a strategic priority.

Second, for both investors and founders, capital discipline is critical. Companies raising under $1M failed at least 78% of the time, but those raising over $100M before failing destroyed the most capital. The sweet spot is $15M–$60M total raised, exiting at $75M–$200M to a strategic acquirer.

The final insight relates to the last. If a ‘great’ exit looks like $200M, then the timing or stage of an investment is critical to return. Earlier stage investors who have good reserves to maintain their position in the winners are the ones that will see return from their AgTech investments.

The original report is freely available here.